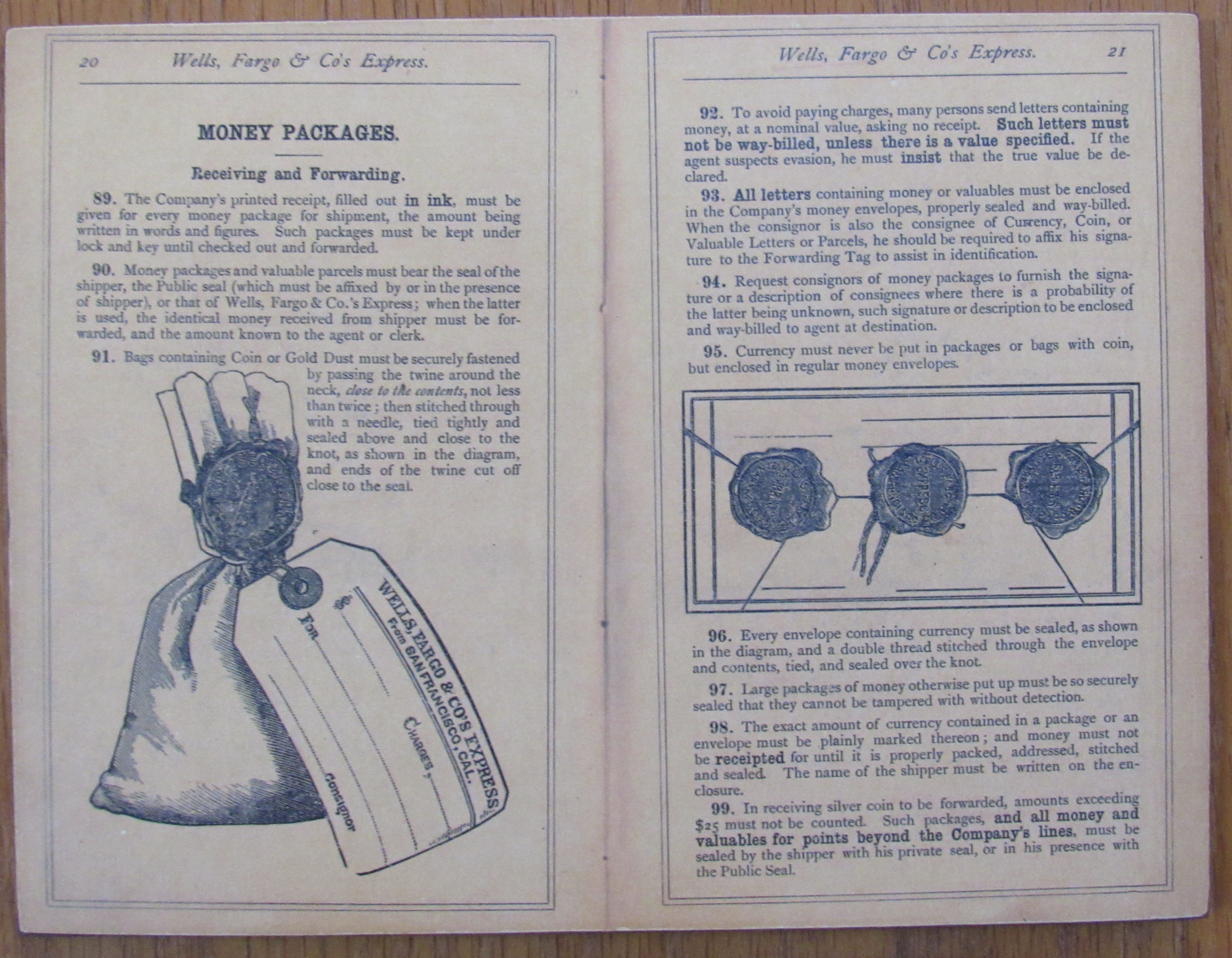

Instructions on how to seal a bag of gold and gold dust for shipping, from the days when Wells Fargo was the gold standard of integrity. Photo by James Ulvog.

There are still a few enforcement actions ongoing over the Wells Fargo fake account fiasco, primarily individual cases against senior officials from a few agencies who haven’t previously settled the charges.

Image doing that to seventy billion dollars. Intentionally. Image courtesy of Adobe Stock.

It is so sad to say, but a reality never-the-less, there are so many major banking fiascos with such a wide range of willing participants that it is impossible to keep straight the players and disasters and fines based just on memory.

So, that means I have a spreadsheet to track the willful disasters I’ve been following.

My tally does not include all the billions of dollars paid to settle mortgage issues arising from the Great Recession. That is another massive set of disasters all by itself.

Here is my running tally of the amount of stockholder equity wasted for a range of different debacles. Amounts in millions of dollars:

There is a long list of banking scandals in the last decade or so with a long list of banks choosing to play in each of the fiascos. Plenty of banks have joined multiple schemes.

The time I’ve allocated to watching the apparently unending disasters has been concentrated on the money laundering and interest rate / exchange rate / pricing manipulation messes, along with the unending variations of cheat-your-customer plans at Wells Fargo.

Until now I’ve not been focused on the bribery disaster involving 1MDB’s shenanigans in Malaysia. If you’ve not tuned in, you can categorize this mess in the international corruption and bribery sector of bank fiascos.

On 10/23/20 Goldman settled up with the U.S. and several other national governments. The bank agreed to clawback $174M from several executives.

They also admitted breaking U.S. corruption laws, specifically with a plea of guilty to charges of conspiring to violate antibribery laws. To keep the parent company in business it was actually a subsidiary of Goldman who entered a guilty plea. Only two executives have been hit with criminal charges.

The feds say billions were stolen from 1MDB and bribes aggregating $1.6B were paid to various government officials around the world.

Financial penalties paid by Goldman:

$2.9B – US Department of Justice and other regulators around the world

From browsing headlines it looks like there are a few other fines but those are in the mere $50M or so range. Chump change for the big banks.

So, five and a half billion dollars of stockholder money burned by bribery and corruption. The irritated populists will loudly remind us that only two executives, merely two, have drawn criminal charges in the U.S.

Concord coach, from the days when Wells Fargo was the undisputed gold standard of honesty and integrity. Photo at Wells Fargo’s San Diego museum by James Ulvog.

The wheels of justice grind slowly, but grind they do.

Wells Fargo agreed to pay the feds three billion dollars for the fake account fiasco. Actually, the board agreed to hand over stockholder’s money.

Also, the feds (specifically OCC) laid sanctions on seven former executives of the bank for their role in the fake account mess.

For those keeping score at home of bank disasters (like me) this settlement is only with the SEC and DoJ and only for the fake account scandal.

The bank also accepted a deferred prosecution agreement and will continue cooperating with the feds over the fake-accounts mess for another three years.

October 2016 photo at Wells Fargo’s museum in San Diego by James Ulvog.

There haven’t been a lot of high-profile articles about the Wells Fargo fake account fiasco recently. I’ve noticed a number of articles though, which suggest there is ongoing activity addressing the intentional, systemic failure. This disaster will not be cleared up soon.

How does Wells fix the indirect harm it caused?

New compensation plan removes cross-selling as a benchmark

Possible MD&A enforcement action?

Branches received 24 hour notice of internal inspections

Bank may eliminate 2016 bonuses for senior staff

12/27/16 – Wall Street Journal – Wells Fargo Is Trying to Fix Its Rogue Account Scandal, One Grueling Case at a Time – Making customers whole will be easy if the customer was only charged a few dollars a month for a while. Still simple to resolve if there were monthly charges and a bunch of overdraft fees because money was taken out of an account unknowingly which resulted in some bounced checks.

What do you do when the unpaid fees on a credit card flowed into negative information on a credit report which resulted in a customer being denied funding for a home loan somewhere else? That’s what happened to one interviewed customer.

Destroying someone’s credit is a tough thing to make right.

A few recent reports: Reason for no criminal prosecution of one too-big-to-fail bank is that it was TBTF, an indictment and a settlement in forex cases, and progress in the money laundering investigations.

Since I use the term a lot, here is a definition of fiasco from Google:

a thing that is a complete failure, especially in a ludicrous or humiliating way. Synonyms: failure, disaster, catastrophe, debacle, shambles, farce, mess, wreck.

Seems to me throwing away $530 million of bank capital because bank staff and leaders wanted to cheat customers meets the definition of fiasco.

7/11 – Francine McKenna at Market Watch – HSBC wasn’t prosecuted because it was ‘too big to fail’: House Committee – A House committee concluded that HSBC wasn’t prosecuted for willful AML violations because it was TBTF. One part of the violations was intentionally leaving out of wire instructions any indication that the funds were related to activity in countries with bans.

Staff recommendations were to pursue a criminal prosecution. Attorney General Eric Holder determined the systemic risk was too high and thus agreed to a deferred prosecution agreement.

Why bank regulators not disclosing the criteria for evaluating “living wills” causes more systemic financial risk

Enforcement efforts on two interest-rate manipulation fiascos

Here is how you get caught for trading on inside information

6/10 – Francine McKenna at MarketWatch – How NASDAQ watches for insider trading – Deep background on how NASDAQ monitors all the trading in the market for suspicious activity. They have a variety of tools and techniques to identify anomalies and drill down to eventually reach the individual trades.

Why was he fired? He merely cost the bank €4.9B back in 2008 after they unwound his unauthorized trades. That is only $5,530,000,000 at today’s exchange rate.

I have a growing interest in ancient finances. Try thinking about how to run a large operation, such as an empire or an army on campaign when there is no banking system and no means of storing wealth other than controlling territory or possessing gold or silver. There is no way to gain any sort of liquidity. Your ability to buy something is limited to the gold in your hand.

How you pay your army today here in the field or buy supplies for 20,000 troops when your wealth is in the form of tons of gold which is a two-month march behind you?

Severe fines against large banks for violating anti-money laundering rules has led the banks to place a heavy focus on making sure their customers are legit. The result is a closing accounts of customers who have too high a risk of being shady. The unintended consequence is legitimate businesses and legitimate charities have difficulty finding a place to do their banking.

In a wonderful irony, articles at The Wall Street Journal on two successive days illustrate the tension. The articles leave you wondering in opposite directions. One article makes you think the banks ought to get serious about screening clients and shut down a bunch of accounts. The other article makes you wonder why these charities doing such wonderful work are getting all their accounts closed for no good reason.

First, charities finding themselves without bank accounts.

Another charity that operates a hospital in Syria had their accounts closed by BofA. After moving to Wells Fargo, their accounts were closed there. Staff at the hospital went four months without pay while the charity tried to figure how to get money into the country.

Authors have spoken to eight other charities who have had their accounts closed. Many others have had money transfers going into Syria, Turkey, or Lebanon held up for varying lengths of time.

Article mentions that banks are under pressure from the U.S. federal government to monitor their customers accounts and close those accounts which could be related to money laundering, whether related to drug running, terrorist financing, or other illegal activity.

Check out this plan for evading money laundering rules. Oh, it came with a money back guarantee to clients whose money was being laundered. Also, I’ve accumulated a preliminary list of industry-wide fines for getting caught busting those AML rules.

11/26 – CNN – Barclays fined $109 million for trying to hide “the deal of the century” – Staff at Barclays came up with a creative plan to hide clients’ money. The staff processed US$2.8B of deposits from “politically exposed people”, meaning people with significant political power and ability to do bad stuff to generate personal wealth.

Commission for the bank was £52M (US$77M).

According to the article, this scheme involved merely performing an Internet search to verify the source of funds as asserted by the clients, did not enter clients’ names on the internal computer systems which meant compliance staff would never find out who owned the money, and used quickly opened & closed offshore accounts to move the money.

In this case, two bankers were indicted for conspiracy and wire fraud for manipulating Libor interest rates while they worked for Rabobank. On November 5 they were convicted by a jury. Therefore we no longer need to use the word allegedly when discussing their manipulation of interest rates.

The newest member of the elite club of banks that write billion dollar checks to settle up with the regulators is Commerzbank AG, the second largest bank in Germany.

After reading several reports on the billion and a half settlement, it seems to me that their corporate culture, at the core personality level, is to be not overly concerned about complying with US law.

The two primary issues are aiding and abetting the billion-dollar Olympus fraud and processing a quarter billion dollars of wire transfers for Iranian and Syrian customers banned from the US banking system.

Not much new reporting in the last week or so on HSBC. There has been a huge amount of political blowback in Europe, especially England. I’m not going into that turmoil.

Irony alert: last article I’ll mention suggests that money laundering may now be illegal in Switzerland, land of the numbered bank account.